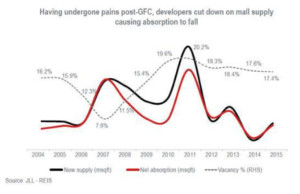

High vacancy in the post-GFC (global financial crisis) years, coupled with a poor consumer and retailer sentiment, led to many developers either deferring launch of proposed retail projects or shelving them altogether. Therefore, the current decade started with falling new supply and demand from retailers.

Post that, there was a period of global economic weakness, coupled with domestic problems pertaining to negative influence of the pre-election uncertainty on business environment as well as controversies surrounding FDI in the retail sector (with a majority of opposition parties trying to oppose opening up of multi-brand retail for FDI), all of which kept the consumer as well as retailer sentiment weak. Also, high consumer price inflation during the 2011-14 period contributed to a poor consumer and retailer confidence.

The general election and its outcome turned out to be a key turnaround moment as a new pro-reforms Government was elected to power with unprecedented majority. This helped many retailers take a positive view on rise in employment numbers, disposable incomes and, therefore, the growth of retail. A gradual softening stance of the newly-elected Government on foreign investment in retail excited international retailers such as IKEA, Walmart etc.

After witnessing a dull period in terms of new supply of Grade-A malls during the previous three years, 2015 saw a remarkable jump in completions. Major completions during the quarter came in the latter half of the year (coinciding with the festival season in India) and included the Mall of India and Gardens Galleria in NCR Delhi, VR Mall in Bengaluru and Acropolis Mall in Kolkata, besides a few others. This time around, malls were experiencing healthy rate of pre-commitments and as a result, their occupancy during commencement was remarkable. Despite rise in completions in 2015, vacancy rate fell across major cities of India.

After witnessing a dull period in terms of new supply of Grade-A malls during the previous three years, 2015 saw a remarkable jump in completions. Major completions during the quarter came in the latter half of the year (coinciding with the festival season in India) and included the Mall of India and Gardens Galleria in NCR Delhi, VR Mall in Bengaluru and Acropolis Mall in Kolkata, besides a few others. This time around, malls were experiencing healthy rate of pre-commitments and as a result, their occupancy during commencement was remarkable. Despite rise in completions in 2015, vacancy rate fell across major cities of India.

Rents get an upward nudge

Mall rents had mostly remained stagnant for most part of the 2012-14 period owing to reasons mentioned above. However, after May-2014 when the elections happened and results were declared, rents started to go up marginally as enquiries from retailers went up.

Tenants prefer superior malls

Tenants prefer superior malls

This period also witnessed a key transition in the organised retail space across major cities. Retailers were now looking for malls that could be classified as quality structures – modern design that promotes good brand visibility, reasonably large floor-plates with ample open areas, professional mall management practices, good upkeep, suitable tenant profile and a good catchment. These factors helped the market to characterise mall properties into three buckets – superior malls, average malls and poor malls.

Over the years, the best retail tenants started to approach only the superior malls, leaving some average malls and poor malls behind in the new cycle of resurgence in retail. Consequently, the vacancy rate in superior malls was under 10 per cent as of year 2015, while average and poor malls were left vacant in the range of 15-40 per cent on an average. Also, in terms of rental values, the superior malls witnessed a sharper rise, while in the average and poor malls, they had even dropped in a few cases. The retail real estate market was in a period of transition where mall quality, average footfalls and trading densities were given higher importance than merely having a retail structure at the right location.

More recently, policies have been announced in favour of the retail sector – 100 per cent FDI in single brand retail, relaxation of sourcing norms for multi-brand retailers, 100 per cent FDI in marketing of food products, the revised Model Shop and Establishment Act (that allows shops to remain open 24×7), bringing in much-needed clarity on “inventory-based” and “marketplace” models in the e-commerce space (giving physical retailers a level-playing field), etc. These policy initiatives have given necessary firepower to the retail sector’s growth in coming years.

More recently, policies have been announced in favour of the retail sector – 100 per cent FDI in single brand retail, relaxation of sourcing norms for multi-brand retailers, 100 per cent FDI in marketing of food products, the revised Model Shop and Establishment Act (that allows shops to remain open 24×7), bringing in much-needed clarity on “inventory-based” and “marketplace” models in the e-commerce space (giving physical retailers a level-playing field), etc. These policy initiatives have given necessary firepower to the retail sector’s growth in coming years.

High vacancy in the post-GFC (global financial crisis) years, coupled with a poor consumer and retailer sentiment, led to many developers either deferring launch of proposed retail projects or shelving them altogether

Must Read